How to File a Supplement After a Claim Is Already Closed

Table of Contents

- What Does "Closed Claim" Actually Mean in Property Insurance?

- Can You File a Supplement After a Claim Is Closed?

- Why Do Insurance Companies Close Claims Prematurely?

- Step-by-Step — How to File a Supplement on a Closed Claim

- Common Situations Where Contractors File Supplements on Closed Claims

- How Claim Supplement Pro Helps You Recover Funds on Closed Claims

-

Frequently Asked Questions About Filing Supplements on Closed Claims

- Can a closed insurance claim be reopened?

- What does it mean when a claim is closed?

- How long do you have to reopen a closed insurance claim?

- Can a contractor file a supplement on a closed claim?

- What is the difference between reopening a claim and filing a supplement?

- What documentation do you need to reopen a closed claim?

- Final Thoughts — A Closed Claim Doesn't Mean Lost Money

Key Takeaways

- “Closed” is a status, not a finality: A closed claim usually means administrative closure. Unless you signed a formal release, you can typically still file a supplement.

- Know your windows: Most policies allow supplements within 1–5 years of the loss, though depreciation recovery deadlines may be shorter.

- Supplements vs. reopening: Filing a supplement is a standard, documentation-driven request for more funds; “reopening” usually implies legal escalation.

- The golden rule of documentation: Always document damage—photos, moisture readings, code references—before repairs begin. Once it’s covered, your proof is gone.

- Common hidden triggers: Supplements are most common for items invisible during the first inspection—roof decking, wall cavity moisture, smoke in ductwork, and missed code upgrades.

- Significant ROI: With professional Xactimate estimating and strong documentation, standard supplements often see a 20–30% increase over the initial payout.

You open up the roof expecting a straightforward repair, and then you see it. The decking underneath is compromised enough that it should’ve been included in the original claim.

The trouble is, the insurance carrier already issued payment based on their estimate and marked the claim as closed. That’s precisely where most contractors or homeowners start assuming the conversation with the insurance company ends, and they either cover the extra cost themselves or are forced to cut corners.

This is also the point where one of the cardinal questions comes up, which is, can a closed insurance claim be reopened?

That assumption is where money gets left on the table. If you want to know what insurance claim supplements are, this guide walks you through how a closed claim still leaves room to recover what was missed.

If you’re sitting on a closed claim with undiscovered damage, Claim Supplement Pro can review it.

What Does "Closed Claim" Actually Mean in Property Insurance?

A closed claim usually means the insurance company evaluated the damage, wrote their estimate, issued payment, and moved on. That’s it.

It doesn’t automatically mean the claim is locked forever or that every dollar related to that loss has been paid.

There are two ways a claim typically gets closed.

Administratively closed

This is the one you’ll see most often in property damage work. The carrier paid based on their scope and marked the file as complete.

No release was signed, and no one waived anything. The claim just hit the end of their internal process.

Closed with a signed release

This one is a bit different. That implies a document like a “Release of All Claims,” where the policyholder agrees not to pursue additional payment. You’ll see this more in auto or injury cases, but it can show up in property claims from time to time.

Now, here’s where doubt winds in. Typically, contractors and homeowners hear “closed claim” and take it as the final step.

However, most property claims have an administrative closure. The carrier finishes their estimate, but they don’t rule on every possible condition behind the walls or under the roof.

Carriers finalize files to keep work progressing, making it a status update, but not exactly a legal decision.

Your ability to request more money comes down to the policy and the clock. Most policies and state rules give you a window to act, often somewhere between one and five years from the date of loss. Depreciation opens up yet another layer.

Some carriers set deadlines to recover it. Miss that window, and you can still submit a supplement, but the depreciation portion may be off the table.

In a nutshell, be aware that closed doesn’t mean finished. More often than not, it simply means no one has asked for more yet.

Can You File a Supplement After a Claim Is Closed?

Yes, in most property damage situations, you can file a supplement on a closed claim. Phrases like ‘can a closed insurance claim be reopened’ and ‘can you reopen a closed insurance claim’ typically point people in the wrong direction, toward legal escalation instead of the supplement process that applies in these cases.

A supplement isn’t the same thing as reopening a claim in the legal sense. Keep in mind that you’re not starting a dispute or bringing in attorneys.

You’re submitting a documented request for additional loss-related funds, based on damage that wasn’t included the first time.

Remember that difference.

Reopening a claim usually points to a formal process involving legal pressure or escalation. Filing a supplement is part of the normal workflow in property restoration.

It happens every day on active and closed files and aligns closely with standard practices for filing and settling homeowners claims.

A supplement makes sense when something was missed, uncovered, or under-scoped, like:

- Hidden damage found during repairs, such as roof decking, wall cavities, or trapped moisture

- Code-required upgrades that weren’t included in the original estimate

- Labor or material costs that were clearly underpriced or incomplete

- Line items that the adjuster didn’t include during the initial inspection

And this is also where many contractors start having doubts about what to do if the claim was underpaid. In most cases, the path forward is building a well-supported supplement.

There are limits. If a formal release was signed or the statute of limitations has passed, your options narrow very fast. Outside of those cases, a closed claim still leaves a possibility to get back what was missed.

Why Do Insurance Companies Close Claims Prematurely?

Most claims aren’t closed because every detail has been fully accounted for. They’re closed because adjusters need to keep files moving.

An adjuster might be coordinating dozens of claims at once, more so after a storm. File closure alleviates that workload, which doesn’t mean the full scope of damage has been captured or priced correctly.

That also partly explains why some adjusters give low estimates. The issue often boils down to limited visibility during the first inspection.

The estimate mirrors what could be confirmed in that moment, not what’s still hidden.

An adjuster typically can’t see:

- Damage beneath shingles, including compromised decking or underlayment

- Water intrusion moving behind the drywall or the ceilings

- Structural problems concealed by finished surfaces

- Moisture or mold developing inside wall cavities

The initial estimate is built from that surface-level view. Hence, it’s just a starting point, but it doesn’t paint the whole picture.

Once work begins, things change. Tear-off and demolition expose what was previously concealed.

Materials that looked intact fail under a more thorough inspection. Areas that seemed unaffected may reveal serious damage.

That rift between the original estimate and the actual condition of the property is where you have to start prioritizing supplements.

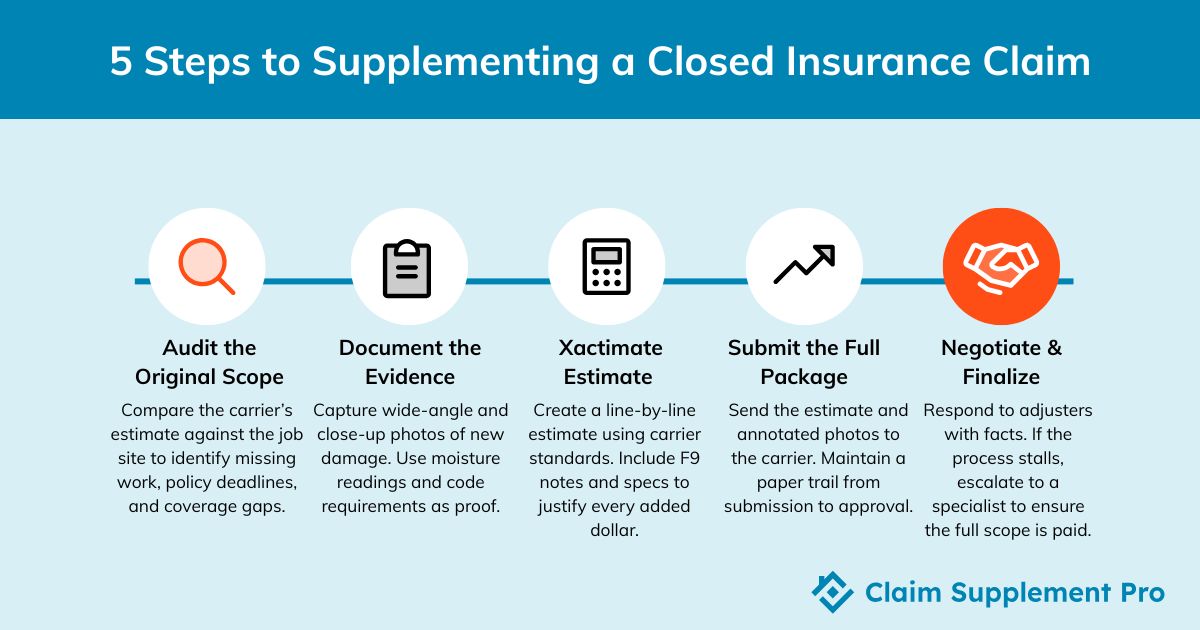

Step-by-Step — How to File a Supplement on a Closed Claim

Step 1 — Review the Original Scope of Loss and Policy

Make the carrier’s estimate your starting point. Pull the Scope of Loss and read it line by line.

Then compare it to what you found once work began. This is where gaps often appear.

Pay attention to what’s missing, and not just what’s underpriced. Look for entire categories of work that weren’t included.

At the same time, check the policy. Deadlines, coverage limits, and depreciation rules all affect how your supplement will be handled.

Don’t forget that you’re developing your case on both the physical damage and the policy language behind it.

Step 2 — Document the Additional Damage Thoroughly

If it’s not documented, it doesn’t exist in the carrier’s eyes.

Take photos that leave nothing out. That means wide shots to depict context and close-ups of the actual issue.

Each damaged area should be easy to identify without explanation.

Use the following to give your photos a stable foundation:

- Measurements that match your estimate to the T

- Moisture readings for water or mitigation claims

- Material details and specifications

- Local code requirements that justify upgrades

Contractor Tip: Take photos before touching anything. Your proof is out the window once the damage is covered or replaced. The rule is to always document first. Then proceed with repairs.

Step 3 — Build a Professional Supplement Estimate

This is the exact point where many supplements succeed or fall apart.

Use Xactimate to create a complete, line-by-line estimate that reflects the additional scope.

Support every item with relevant evidence. Measurements must match your documentation, while notes should explain why each line is there.

Include:

- F9 notes that justify added items

- Code references where upgrades are required

- Manufacturer specs when relevant

- Subcontractor bids if part of the scope

Strong estimating services make a huge difference here. An experienced estimator knows which line items tend to get missed, and how to lay them out in a way adjusters recognize and approve.

Step 4 — Submit the Supplement to the Carrier

Reach out to the carrier and reference the original claim number. Keep it straightforward.

Send a complete package:

- Updated Xactimate estimate

- Annotated photos

- Code documentation

- A short explanation of the added scope

Submit everything in writing. Email works, especially with a read receipt. Some carriers prefer their online portals.

Either way, keep records.

You want a neat paper trail from the first submission to final approval, especially in situations where ‘can a closed insurance claim be reopened’ becomes part of the broader claim conversation.

Step 5 — Manage the Negotiation and Follow-Up

Expect questions once you submit it. Adjusters may ask for clarification or request more documentation.

Respond quickly and stay focused on the facts. A single delay is sufficient to hamper payment.

It helps to work from a supplement documentation checklist so you don’t miss anything during follow-up. After all, if you miss just one piece of support, you risk halting the entire process.

If the back-and-forth drags or the pushback doesn’t line up with the documentation, escalate. Ask for a supervisor or bring in a supplement specialist who deals with carrier negotiations every day.

Common Situations Where Contractors File Supplements on Closed Claims

A closed file doesn’t change what’s happening on-site. Once work begins, the real scope starts to show, and it often goes beyond the original estimate.

That’s the gap contractors deal with every day.

Here are some of the most common situations where supplements come up:

- Roofing: Shingle tear-off exposes what the initial inspection couldn’t. Damaged decking, missing or inadequate underlayment, and failing flashing tend to show up fast. These are some of the most frequently missed damage items in residential storms, simply because they sit beneath the surface.

- Water Mitigation: Drying equipment does its job, but it also reveals how far moisture traveled. Wall cavities, subfloors, and areas behind baseboards often hold damage that was initially out of sight. Mold can also form in places that looked unaffected during the initial walkthrough.

- Siding: Removing damaged panels can uncover complex issues like deteriorated sheathing or failed building wrap. This is how what looked like a surface repair turns into a larger scope once the structure is exposed.

- Fire Restoration: One thing is certain – smoke doesn’t stay in one place. It moves through ductwork, insulation, and hidden structural areas. Initial inspections tend to miss how far contamination has spread, especially in enclosed systems.

- Code Upgrades: Local building codes don’t adjust to match an estimate. Requirements like ice and water shield, proper ventilation, or updated insulation standards often weren’t included the first time around.

All of this goes back to a simple point. Understanding property insurance claims, including what it means when a claim is closed, aids contractors in recognizing that a closed claim only demonstrates what the carrier could see initially. But it doesn’t mean the property stopped revealing damage.

How Claim Supplement Pro Helps You Recover Funds on Closed Claims

Claim Supplement Pro steps in where most claims collapse, after the initial estimate leaves disparities between what was reimbursed and what the job requires.

It starts with an exhaustive analysis. The original Scope of Loss is compared against real jobsite conditions, line by line.

Missed items, under-scoped work, and code requirements are all identified before anything is submitted.

From there, the team builds a complete, code-compliant Xactimate estimate. This includes precise line items, F9 notes that account for each addition, and supporting documentation that holds up under scrutiny. That’s why solid estimating services are so indispensable, especially when the goal is to present the scope in a way adjusters can’t easily dismiss.

Just as important, Claim Supplement Pro tackles the entire communication flow. The back-and-forth with the adjuster, requests for clarification, and the negotiation process are all taken care of so contractors can focus their attention on the jobsite.

Timing is also critical. Policy deadline awareness is built into the process, so you can rest assured that supplements are filed within the allowed window and depreciation opportunities aren’t missed.

Many closed claims sit untouched because of confusion around whether additional funds are still recoverable. In practice, claims can often be reopened with proper documentation and a well-built supplement.

The results speak for themselves. Standard claims often see increases in the 20–30% range, with higher recoveries when documentation is strong. For a real example, see how we recovered $6,057 in hidden damage and code upgrades on a residential roof claim — exactly the kind of hidden-scope discovery this guide describes.

Have a closed claim with hidden damage? Contact Claim Supplement Profor a claim review.

Frequently Asked Questions About Filing Supplements on Closed Claims

Can a closed insurance claim be reopened?

Yes — in most property damage cases, a closed claim can be supplemented with additional documentation. The carrier may have closed the file administratively, but that doesn’t eliminate your right to request additional payment for legitimate damages discovered after the initial estimate.

What does it mean when a claim is closed?

A closed claim means the insurance company considers its current obligation fulfilled based on what was documented. It’s a file status, not a final legal ruling. If new damage is found that relates to the original loss, a supplement can be filed to request that the claim be reviewed again.

How long do you have to reopen a closed insurance claim?

Timeframes vary by state and policy. Most states allow supplemental filings within 1–5 years of the date of loss. Check your specific policy language and consult your state’s department of insurance for exact deadlines. Act quickly — physical evidence degrades over time.

Can a contractor file a supplement on a closed claim?

Yes. Contractors regularly file supplements when they discover additional damage during repairs. The contractor prepares the documentation, builds the Xactimate estimate, and submits it to the carrier on behalf of the property owner.

What is the difference between reopening a claim and filing a supplement?

Reopening a claim typically involves a legal or formal dispute process — often handled by attorneys or public adjusters. Filing a supplement is a documentation-driven process where you present evidence of additional damage and request that the carrier approve more scope. Supplements are standard industry practice.

What documentation do you need to reopen a closed claim?

At minimum: the original Scope of Loss, photos of the additional damage (before and after), a revised Xactimate estimate with line-item detail, applicable building code citations, manufacturer specifications, and a written narrative explaining why additional funds are justified.

Final Thoughts — A Closed Claim Doesn't Mean Lost Money

A closed claim is just a file status, and can be far from the damage’s full value.

There’s still a path to recover the costs if new issues arise after the original estimate. Supplements exist for exactly that reason.

The difference comes down to how well you document and present the damage.

Clear photos, accurate Xactimate estimates, code references, and a solid explanation of the added scope all work together to support the claim.

Don’t let a closed file turn into lost revenue or out-of-pocket costs. Not sure if your closed claim qualifies for a supplement? Let Claim Supplement Pro review it.