ACV vs RCV in Insurance Claims: What Contractors Need to Understand

Table of Contents

- ACV vs RCV: The Two Payment Types Contractors Typically See

- How Do I Know If I Have RCV or ACV Coverage?

- How Depreciation Works (and Why It Matters for Your Cash Flow)

- The Two-Check Process Most Contractors Deal With

- ACV vs RCV Side-by-Side: A Contractor's Comparison

- How Do I Know What Does RCV and ACV Mean on an Insurance Claim Estimate?

- A Realistic Example: How the Numbers Break Down

- How Supplements Interact With ACV and RCV Payments

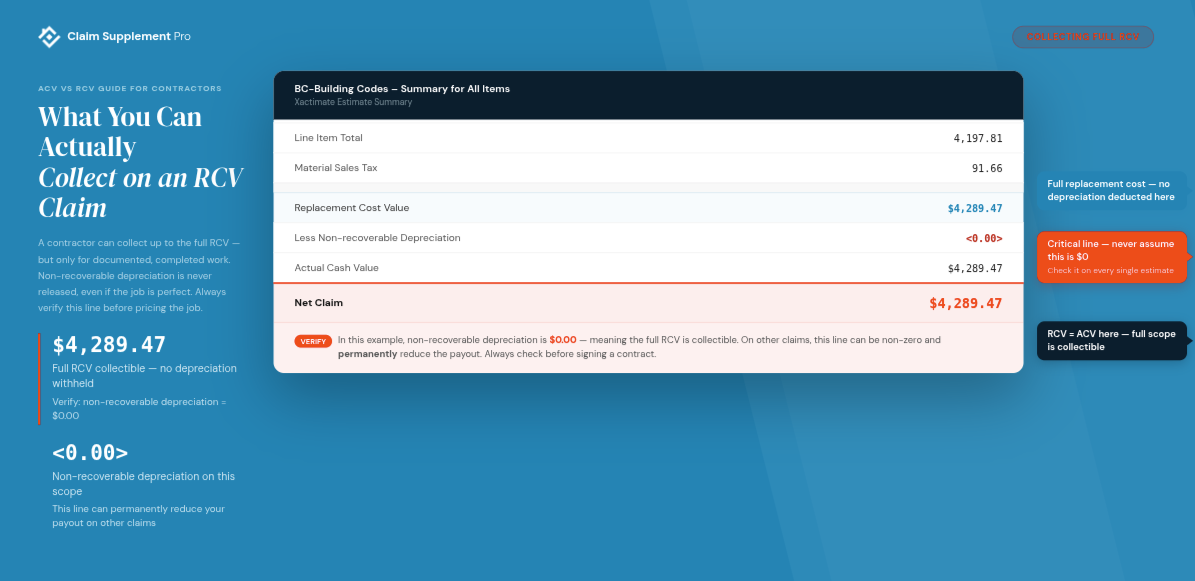

- How Much Can a Contractor Collect on an RCV Claim?

- Common Mistakes Contractors Make With ACV and RCV Claims

- Frequently Asked Questions

- Final Thoughts: Why ACV vs RCV Matters More Than Most Contractors Realize

Key Takeaways

- ACV vs. RCV in one line: ACV is the depreciated upfront payment; RCV is the full cost to complete the work with like-kind materials and proper scope.

- The two-check reality: Most claims pay ACV first, then release recoverable depreciation after the job is completed and documented—creating cash flow pressure between checks.

- Check the declarations page before signing: Some policies default to ACV, especially on older roofs or with wind and hail endorsements. Confirm coverage type upfront to avoid mid-job surprises.

- Documentation triggers the second check: A final invoice matching the approved scope, completion photos, material receipts, and permit records are what release recoverable depreciation.

- Supplements move both numbers: Every approved supplement raises the RCV, which lifts the ACV payment and the depreciation release. Incomplete scopes shrink the job twice.

- Non-recoverable depreciation is gone for good: No matter how clean the documentation is, that portion stays deducted—plan margins accordingly.

There’s hardly a contractor who hasn’t encountered a situation where the first insurance check comes in, and it doesn’t cover the materials–let alone labor and overhead. That payment is almost always based on Actual Cash Value (ACV), and if you don’t understand how it’s calculated and what comes next, the job can quickly go from a profitable project to a burden on your finances.

Keep in mind we’re not talking about policy definitions or legal language. From a contractor’s perspective, insurance RCV vs ACV is about timing, documentation, and getting compensated for the work’s full scope.

The structure of these two payment types directly affects how you schedule production, manage receivables, and decide when to push for supplements.

This article will break down what ACV and Replacement Cost Value (RCV) mean in day-to-day operations, how the two-check process works, and how depreciation is recovered.

We’ll also explore the connection between these payments and what insurance claim supplements are in practice to show how scope accuracy and documentation contribute to the initial check and the final release.

ACV vs RCV: The Two Payment Types Contractors Typically See

When we probe into the practical level, the majority of property claims come down to two numbers that contractors need to track. ACV and RCV.

However, you have to understand more than insurance RCV vs ACV definitions, and know how and when money moves through a job.

For many contractors reviewing estimates for the first time, what RCV and ACV mean on insurance claim paperwork becomes obvious only when those numbers are directly related to real job costs and payment timing.

- ACV (Actual Cash Value) is the reduced, depreciated amount paid upfront.

- RCV (Replacement Cost Value) is the full cost to complete the work with like-kind materials and adequate scope.

Most claims involve both at different stages. The initial payment is typically based on ACV, while the remaining balance (the one depreciation-related) is released later once the work is completed and documented.

That structure has a role in how you fund materials, schedule crews, and manage receivables.

Contractors know that the difference between ACV vs RCV on an insurance claim isn’t theoretical. In fact, it determines whether a job can support itself financially or requires you to float costs while waiting for the second payment.

What Does ACV Stand for in Insurance?

ACV stands for Actual Cash Value, which is the replacement cost of the damaged property minus depreciation.

In simple terms, carriers start with what it would cost to replace the roof, siding, or interior finishes today, then subtract value based on age, condition, and expected lifespan. The result is the ACV payment, the amount issued in the first check.

This is why the initial payment often feels low. It’s not really designed to cover the full scope of work, only the depreciated portion of it.

If you’re a contractor, that means the ACV check typically funds materials and a portion of early labor, yet rarely the entire job.

What Is RCV in Insurance?

RCV stands for Replacement Cost Value, which represents the full cost to repair or replace damaged property using like-kind and quality materials.

This is the number contractors build their estimates around. It matches the real cost of completing the job based on accurate scope, current pricing, and all required trades.

The divide between ACV and RCV is depreciation. That withheld amount can be released once the work is completed and properly documented. Hence, from a contractor’s standpoint, RCV is the target because it aligns with what it takes to finish the project and close out the job without leaving out revenue.

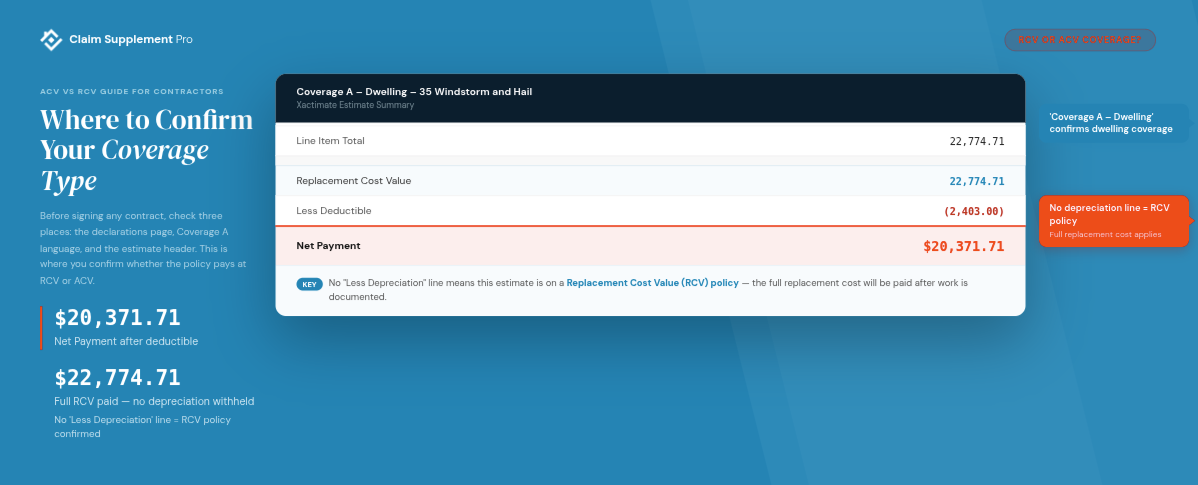

How Do I Know If I Have RCV or ACV Coverage?

Before starting any job, contractors need to confirm how the claim will be paid because ACV vs RCV coverage impacts how the project gets funded. That’s why you need a more comprehensive knowledge of the insurance claim RCV vs ACV in real scenarios.

You can usually find this in three places. The declarations page will outline whether the policy pays at Replacement Cost Value or Actual Cash Value.

The Coverage A (Dwelling) section often includes “Loss Settlement” language that explains whether depreciation is recoverable. And the estimate header in the carrier’s scope may also show whether the numbers are based on ACV, RCV, or both.

Some policies default to ACV, more so for older roofs or when specific wind or hail endorsements apply. That’s why two similar claims can have very different payouts.

Contractor tip: Always ask to evaluate the declarations page before signing a contract. It's the best way to bypass surprises once the job has already begun.

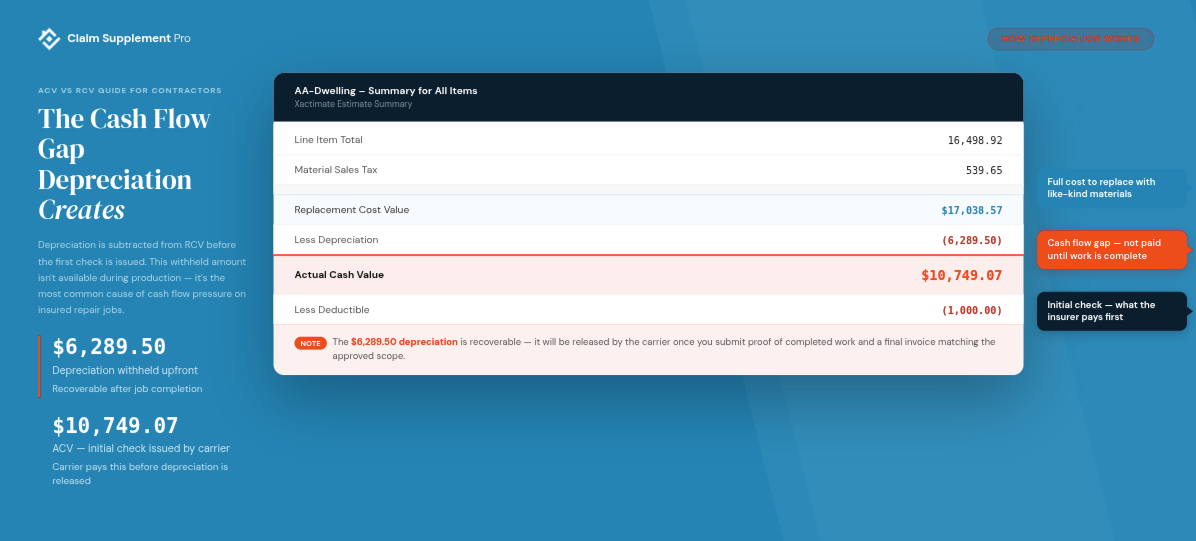

How Depreciation Works (and Why It Matters for Your Cash Flow)

Depreciation is the difference between ACV and RCV, and for contractors, it’s the piece that often decides whether a job runs steadily or triggers a cash flow squeeze.

In simple terms, depreciation is the value carriers subtract from the replacement cost based on age and condition. Age depreciation mirrors how far along a material is in its expected lifespan, while condition depreciation accounts for wear and overall state at the time of loss.

Both appear as line items in the estimate and lower the initial payment.

The critical distinction is whether that depreciation is recoverable or non-recoverable. Recoverable depreciation can be paid later, once the work is completed and documented.

Non-recoverable depreciation remains deducted–meaning it will never be released regardless of what happens on the job.

Depreciation is applied at the line-item level in Xactimate and rolled up into totals that impact ACV and RCV figures equally. If you’ve worked through any Xactimate estimating guide for contractors, you’ve probably seen how these categories influence the bottom line, especially when different trades or materials come with different depreciation rates.

This isn’t a contractor-versus-carrier issue, but rather how the policy is structured. The key for contractors is grasping how depreciation affects funding at each stage and making sure the scope matches the required work correctly.

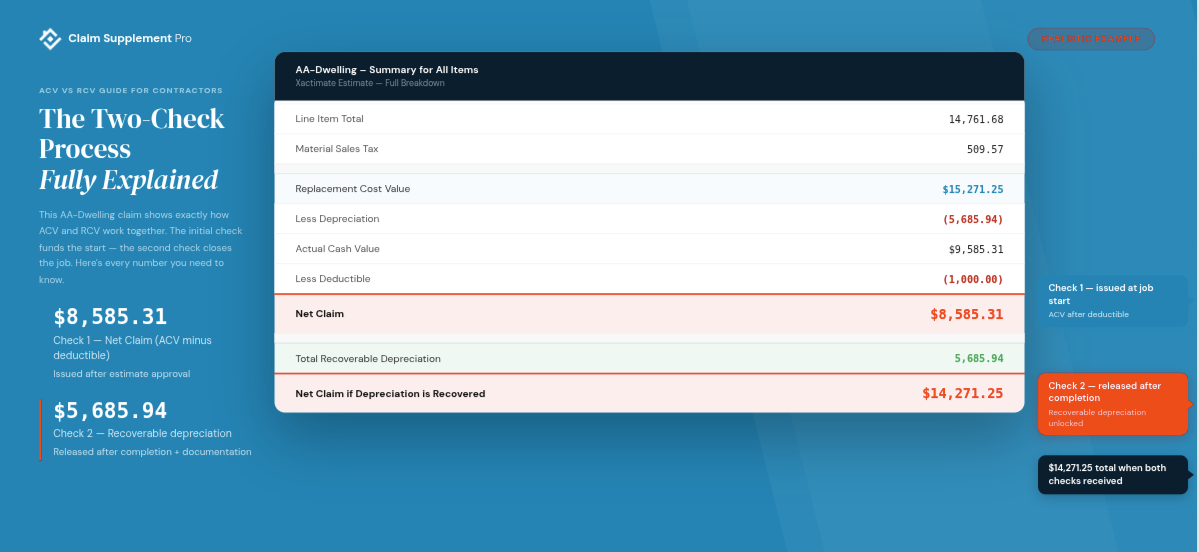

The Two-Check Process Most Contractors Deal With

Most property claims follow a two-check structure, and it’s about how the insurance carrier handles depreciation.

- Check 1: ACV payment. This includes an upfront issuance after the initial estimate approval. It’s the sum of the replacement cost minus depreciation, which is why it often comes in below the full project cost.

- Check 2: Recoverable depreciation. This is released after the work’s completion and proper documentation. It closes the difference between ACV and RCV.

The timing between these two payments can vary. In some cases, the contractor submits proof that the job is finished, and the second check follows almost right after.

In others, delays happen when the documentation is incomplete or doesn’t match the approved scope.

This delay creates cash flow pressure. You’re often expected to advance with production while a portion of the total claim value is still pending. But it’s easy for jobs to drag or require extra working capital to progress without an explicit understanding of how and when that second payment is triggered.

For a deeper look at how supplement support shortens these timelines, see our guide on how third-party supplementing helps restoration GCs get paid faster.

ACV vs RCV Side-by-Side: A Contractor's Comparison

| Factor | ACV Payment | RCV Payment |

|---|---|---|

| When paid | Upfront, after initial estimate approval | After work is completed and documented |

| What it represents | Replacement cost minus depreciation | Full replacement cost |

| Documentation needed | Estimate, photos, scope | Final invoice, completion photos, proof of work, code compliance docs |

| Contractor impact | Funds material and initial labor | Closes out the job and releases full margin |

| Supplement timing | During the review of the initial estimate | Before final invoice submission |

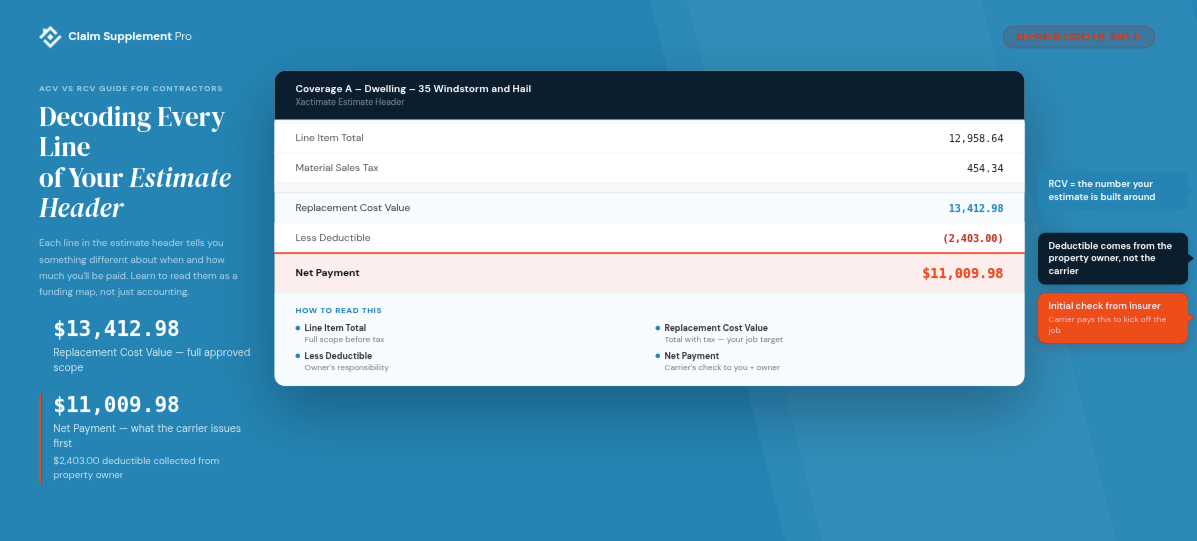

How Do I Know What Does RCV and ACV Mean on an Insurance Claim Estimate?

When contractors ask what does RCV and ACV mean on an insurance claim, the answer is usually sitting right in the estimate header. The challenge is knowing how to read those numbers in a way that matches real job costs.

These numbers are the practical breakdown behind insurance RCV vs ACV and how each payment is structured.

In an Xactimate estimate, you’ll typically see:

- RCV (Replacement Cost Value): the full approved scope before any deductions

- Depreciation: the amount subtracted based on age and condition

- ACV (Actual Cash Value): RCV minus depreciation

- Deductible: the portion the property owner is responsible for

- Net claim: what the carrier actually pays after depreciation and deductible are applied

RCV is the full job value you’re working toward. ACV shows what funding is available upfront.

The deductible affects what needs to be collected from the customer, not the carrier.

Together, they show how RCV vs ACV on an insurance claim plays into both the first check and the final payment.

Some may find it bewildering how these numbers interact. ACV is often shown after the deductible, which can make the first check look even smaller.

Non-recoverable depreciation won’t be paid later, even after completion. Carriers may include or exclude overhead and profit depending on the scope and trades involved.

A Realistic Example: How the Numbers Break Down

Let’s look at a simplified residential roof claim to see how this plays out in practice. This is an illustrative example, so don’t take it as a guaranteed outcome.

- RCV (full roof replacement): $15,000

- Depreciation: $5,000

- ACV: $10,000

- Deductible: $1,000

- Initial payment (ACV minus deductible): $9,000

In this scenario, the contractor starts the job with $9,000 from the carrier, plus the deductible collected from the homeowner. The remaining $5,000 in depreciation is recoverable, but only after the work is completed and verifiable.

That means there’s a $5,000 portion of the total job value that isn’t available during production. Contractors need to plan around that timing, especially for materials and labor, as well as scheduling.

Once the project ends and the final invoice is in line with the approved scope, the insurance carrier can release recoverable depreciation, bringing the total paid amount up to the RCV.

For a complete walkthrough of supplementing on the roof scenarios this example illustrates, see our step-by-step roof supplement guide.

How Supplements Interact With ACV and RCV Payments

Supplements update both the ACV and RCV figures in the claim. A missing line item reduces the RCV total, yet it also lowers the ACV payment and the amount of depreciation that can be recovered later. That’s why incomplete scopes affect the job twice.

Effectively, insurance claim supplements come down to adding and documenting the scope that mirrors the total needed work. After the dispensation of the initial estimate, supplements are typically submitted to address missing trades, code-required upgrades, or items that weren’t included in the carrier’s scope.

This step is critical for aligning the RCV with the job’s real costs before production moves too far forward.

Supplements can also happen during or after production. Tear-off may disclose previously concealed layers, damaged decking, or installation requirements that weren’t visible during the initial inspection.

Material availability changes or code enforcement discovered during permitting can also require updates to the scope.

Every approved supplement adjusts the RCV total, which in turn affects the ACV payment and the final depreciation release. The more accurate the scope, the more predictable the funding.

At every stage, documentation is what drives the outcome, as it supports the initial payment, validates supplements, and keeps the final reconciliation in line with the work performed.

The Documentation That Triggers a Clean RCV Release

A smooth depreciation release depends on how well the completed job matches the approved scope on paper.

That starts with a final invoice that aligns line by line with the estimate, including any approved supplements. Completion photos should clearly support the work performed and tie back to specific line items. Material receipts and manufacturer documentation help confirm that like-kind and quality requirements were met.

In addition, permit and inspection records show that the work meets local requirements, while communication logs with the adjuster provide context for any scope changes or approvals along the way.

Incomplete or inconsistent documentation is the most common reason depreciation releases are delayed or reduced. The final payment becomes harder to process when the paperwork is in dissonance with the scope, even if the work itself is complete.

How Much Can a Contractor Collect on an RCV Claim?

A contractor can collect up to the full replacement cost on an RCV claim, but only for work that is completed and comes with documentation.

The approved scope drives the total payout. Every line item in the estimate contributes to the initial ACV payment and the recoverable depreciation related to it.

If something is not within the scope, it won’t be included in either payment.

We also have to account for non-recoverable depreciation, which is never released. This can apply to older roofs, certain wind or hail endorsements, or specific policy limitations.

In those cases, part of the depreciation is permanently deducted, regardless of project completion.

The takeaway is simple for contractors. The accuracy of the line-item scope in Xactimate dictates how much of the RCV can be collected at the end of the job.

For a real example of scope accuracy translating to recovered value, see how we recovered $9,361 on a residential roof claim — a 70% increase over the warranted estimate.

Common Mistakes Contractors Make With ACV and RCV Claims

Contractors often run into issues because they handle the payment structure incorrectly throughout the job.

Many treat the ACV check as the final payment and skip the documentation needed to trigger the depreciation release. Others fail to track which line items carry recoverable versus non-recoverable depreciation, which leads to incorrect expectations about the final payout.

Some submit a final invoice that doesn’t match the approved scope, causing delays or the RCV release blocks.

Contractors also assume all policies are RCV and skip analyzing the declarations page before signing.

In situations where scope and numbers don’t align, following a straightforward process for what to do if your insurance claim was underpaid becomes part of managing the job correctly.

Frequently Asked Questions

Is RCV Better Than ACV for Contractors?

In most cases, yes–but only when documentation and supplements are handled correctly. Poorly documented RCV claims can still result in lower final payouts if the full scope isn’t captured and approved.

How Is ACV Calculated on an Insurance Claim?

ACV is calculated as RCV minus depreciation. Carriers apply depreciation based on age, condition, and expected useful life of the materials.

Do You Have to Pay Back RCV If You Don’t Use It?

No, because depreciation is only released for completed and documented work. If the full scope isn’t completed, that portion simply isn’t paid out.

Can a Contractor Collect Recoverable Depreciation Directly?

It depends on the state, the policy, and whether a direction-to-pay or assignment of benefits is in place. Always follow local regulations and policy terms.

Does Insurance Pay ACV or RCV First?

ACV is paid first. The remaining depreciation is released after the job is completed and documented.

What Is an Example of Actual Cash Value?

If a roof has a replacement cost of $12,000 and $4,000 in depreciation, the ACV would be $8,000 before the deductible is applied.

Final Thoughts: Why ACV vs RCV Matters More Than Most Contractors Realize

The difference between insurance RCV vs ACV dictates whether a job funds itself or creates pressure on your working capital. You should understand how each payment works to plan production, manage cash flow, and steer clear of unexpected situations during the project.

But it all revolves around the scope’s factuality and evidence. The initial ACV payment and the final depreciation release are always easier to anticipate when you have a precise estimate.

For that, you need professional estimating services that can help you build a robust scope that supports the claim from the get-go and maintains the job aligned through completion.

If you’re dealing with stalled depreciation releases or scopes that don’t match the job requirements, Claim Supplement Pro’s estimating team can help you get the full recoverable value documented and approved. Contact us for a claim review.